The Five Instinctual Behaviors of Financially Squeezed Americans

Latest

ELI Reports

The Five Instinctual Behaviors of Financially Squeezed Americans

On May 9, the University of Michigan consumer sentiment indexed closed at 49.8 — the lowest reading in the survey's 74-year history. Three of the four worst sentiment numbers ever recorded have now happened in the past nine months. Gas in California crossed $6 a gallon after the Iran conflict pushed Brent crude past $100. Tech employers have cut more than 100,000 white-collar jobs this year alone, and the long-term unemployed has grown by 322,000 over the past twelve months. The economic consensus reads it as a single story: Americans are pulling back.

The behavioral data tells a different story. Sooth analyzed the signals of America’s financially anxious middle — adults earning $40K to $200K, holding multi-category discretionary lives, and currently carrying multiple money worries — and found that financial pressure does not produce a single consumer behavior. It produces five.

When confidence drops and finances get tight, Americans split into five instinctual coping modes — each one a different strategy for surviving a squeeze. Each one rewards a different kind of business. And each one is invisible to the income-and-demographic frameworks every major retailer, bank, and policymaker is still using to plan the next twelve months.

In The Frame:

- 49.8%: University of Michigan consumer sentiment as of May 2026 — a 74-year low

- $6: Average California gas price after the Iran war pushed global oil prices past $100

- 100k+: White-collar jobs cut in 2026, even as official unemployment sits at 4.3%

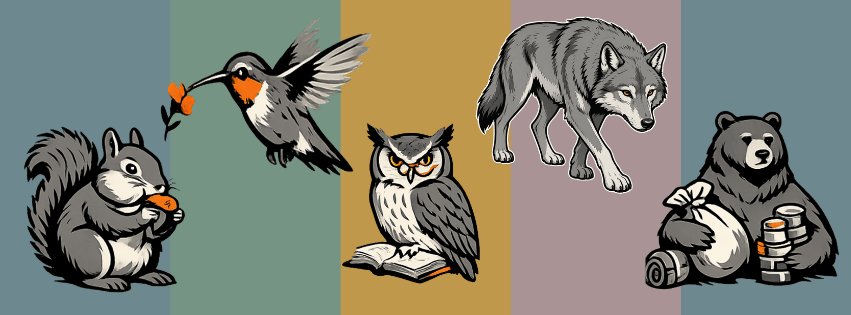

Where do they turn when their finances get tight?

Financially anxious middle-income Americans, segmented by how they cope

Squirrels: 53%

- Pragmatic family protectors: stretch the dollar, splurge selectively, stay calm.

- 75% more likely than average to see themselves as savers and 64% more likely as “thrifty parents" budgeting for family.

- Grocery shopping is a value-and-essentials playbook — visits dollar stores, supercenters, and discount grocers at twice the national rate.

- Active debt management shows over a third plan a major loan payment within six months.

- The Squirrel rewards value grocery, dollar stores, and family-protection brands.

Hummingbirds: 20%

- Aspirational improvisers in constant motion.

- The only segment where working students are more than twice as likely to be in school and working part-time simultaneously.

- Lives on fintech and peer-to-peer payments, displacing traditional accounts at twice the national rate.

- Aspirational department stores like Macy’s, Nordstrom, and Bloomingdale’s persist despite tight budgets, reaching one in five. The Hummingbird rewards fintech banking, value-tier QSR, and aspirational-accessible fashion.

Owls: 13%

- Methodical financial repositioners. Read, study, and quietly move the money.

- Read serious financial media over twice as often as average Americans, including Bloomberg, The Economist, Barron’s, and Businessweek.

- Three times more likely to have accounts at major investment houses and self-managed platforms.

- Banking is dynamic, not panic-driven — among the most likely Americans to leave a major bank last year. The Owl rewards financial advisory services, brokerage platforms, and banking alternatives.

Wolves: 8%

- Risk-tolerant speculators. If the wage isn’t enough, the bet has to be bigger.

- Over three times more likely to actively trade on retail and crypto platforms — speculation is the strategy, not a hobby.

- Almost half cite job security as a top fear — the highest among squeezed-American segments—likely due to wage anxiety.

- Daily spending centers on gas stations, drive-thrus, and convenience stores, with affinity for value-tier QSRs near four times the national average. Wolf rewards crypto, trading platforms, convenience retail, and betting apps.

Bears: 5%

- Bulk-buying long-horizon hedgers. Buy deeper, slower, and ahead of the squeeze.

- Warehouse-club shopping is six times the average — bulk dominates grocery strategy.

- Hedging across asset classes is a key financial behavior, with individuals four times more likely to hold crypto on alternative exchanges while deeply engaged with traditional investing media.

- Heavy adopters of fintech banking and payment apps at four times the national rate. The Bear rewards warehouse clubs, fintech banking, and alternative investing platforms.

How will American consumers' coping strategies play out across industries?

1. Warehouse clubs and dollar stores will post the biggest retail wins of 2026.

The Squirrel dominates the squeezed American market, favoring dollar stores, super centers, and discount grocers, with occasional splurges. Bears stockpile at warehouse clubs, concentrating consumer spending in these formats. Costco, Sam’s Club, BJ’s, Dollar General, Dollar Tree, and Aldi are expected to outperform traditional grocers and big-box retailers through Q4. Mid-tier specialty grocery without a clear value or premium identity will suffer.

2. FinTech banking will take a generational leap in market share.

Owls are abandoning traditional banks, and hummingbirds never came. Bears are migrating to Chime, Current, and new payment systems. Wolves rely on Cash App as their main account. The trend across most instincts shows the decline of traditional banks, with competitors gaining from this shift. Expect record customer growth for Chime, SoFi, Current, Cash App, and Capital One, while regional and mid-tier banks face significant pressure since 2008.

3. Cypto and betting platforms will grow in an economy that looks like it should shrink them.

The Wolf trades because of financial anxiety, not despite it. With job security fears and flat wages, many Americans turn to speculation. While conventional wisdom says volatile assets sell off at sentiment lows, behavioral data shows active retail engagement increases in platforms like Robinhood, Coinbase, DraftKings, FanDuel, and prediction markets. Expect regulatory friction as this trend becomes visible.

4. Value-tier QSR will beat fast-casual for the first time in a decade.

The data shows fast-food brands like Taco Bell, McDonald’s, Wendy’s, Subway, and Burger King dominate, reaching one in five Hummingbirds and Wolves, and over one in seven Squirrels. In contrast, Chipotle, Sweetgreen, Cava, and the fast-casual segment lack significant presence in U.S. segments. Fast-casual growth is plateauing, and brands such as McDonald’s, Yum! Brands, and Restaurant Brands International are expected to surpass fast-casuals in sales through 2026. Any quick-service concept with an average check above $12 is at risk.

5. The aspiration economy will survive the squeeze — just not where Wall Street expects.

Hummingbirds shop at Macy’s, Nordstrom, and Bloomingdale’s despite tight budgets. Squirrels splurge on Whole Foods and Marriott while shopping Dollar Tree. The desire to dress well and indulge in small luxuries persists under financial pressure—just more focused. Department stores, seen as dying, will show resilience in 2026. The top 1% luxury market will hold; middle-tier aspirational goods will struggle, as instincts do not reward them.

DATA SOURCES FOR THIS EDITION OF THE ELI REPORT

Insights are based on Sooth’s patent-pending methodology, which analyzes over 100 million intent signals from 220 million anonymized US adults to predict, with 91% accuracy, how their emotional, practical, and situational needs will influence their buying decisions and the subsequent impact on people, businesses, and the economy. In addition, the following sources were used for corroborating data and the qualification of predictive insights:

Consumer sentiment index 49.8, May 2026: University of Michigan Surveys of Consumers, May 9, 2026 · California gas prices above $6/gallon, Brent crude at $100: Goldman Sachs Energy Research, May 7, 2026; AAA Fuel Gauge Report, May 2026 · Tech sector layoffs, 100K+ workers in 2026 YTD: SkillSyncer Layoff Tracker, May 2026 · March 2026 employment, 4.3% unemployment: US Bureau of Labor Statistics, April 3, 2026 · Long-term unemployed +322K YoY: US Bureau of Labor Statistics, April 2026 · K-shaped consumer spending divergence: Bank of America Institute Consumer Checkpoint, January 2026 · Inflation expectations, gas and grocery price expectations: Deloitte ConsumerSignals, April–May 2026 · Audience definition: US adults earning $40K–$200K, owning at least one vehicle, engaged in three or more discretionary categories (streaming, restaurants, beauty, travel, music, theater, pets, fitness, apparel, hobbies, sports), and expressing at least two of these fears: job security, cost of living, retirement savings, tax increases · Behavioral segmentation: Sooth sample of 35.5M American adults, May 2026, segmented across content affinity, financial services, retail and grocery behavior, media consumption, and psychographic signals

About Sooth & ELI

Sooth is the predictive intelligence company decoding the 93% of human decisions driven by emotional, practical, and situational needs. Powered by ELI — Sooth's exclusive Emotional Logic Interface — Sooth uncovers hidden signals, turning audience behavior into predictive foresight. Sooth's patent-pending methodology uses artificial intelligence to cross-reference more than 100 million intent signals with data on 300 million individuals worldwide to predict buyer tendencies with 91% predictive accuracy. For more information, visit: soothbetold.com.

Subscribe to the ELI Report

Enjoyed these insights? Subscribe now and get actionable tips delivered to your inbox every other week—giving you an edge over your competitors.

Original source:

Click here to read more